This year, Wall Street has viewed Apple as opportunity cost.

The Street has cared mostly about AI. Non-AI stocks – even outstanding companies like Apple and Costco – have been sold as a source of funds.

But the success of the iPhone 17 is breathing life back into Apple. And in a market focussed on AI, Tim Cook’s buyback machine is starting to look cheap.

iPhone 17: Apple’s revival engine

In Q2, things looked awful for Apple.

Trump’s tariffs threatened margins. Google’s fat search payment was under legal attack. Expectations for the iPhone 17 were low.

Yet Apple, and Tim Cook, won virtually everything.

In September, courts said Google could keep paying Apple to be the iPhone’s default search engine. That payment – roughly US$25 billion a year with no attached costs – is one of the biggest gold mines in tech.

On tariffs, Cook largely won his negotiations with Trump. In exchange for a modest hiring pledge, he secured a full exemption. Competitors were less lucky. Samsung faces a 15% tariff, Xiaomi a crippling 54%. As the iPhone was exempted from Chinese counter tariffs, tariffs have emerged as net positive for Apple, protecting its margins on home soil.

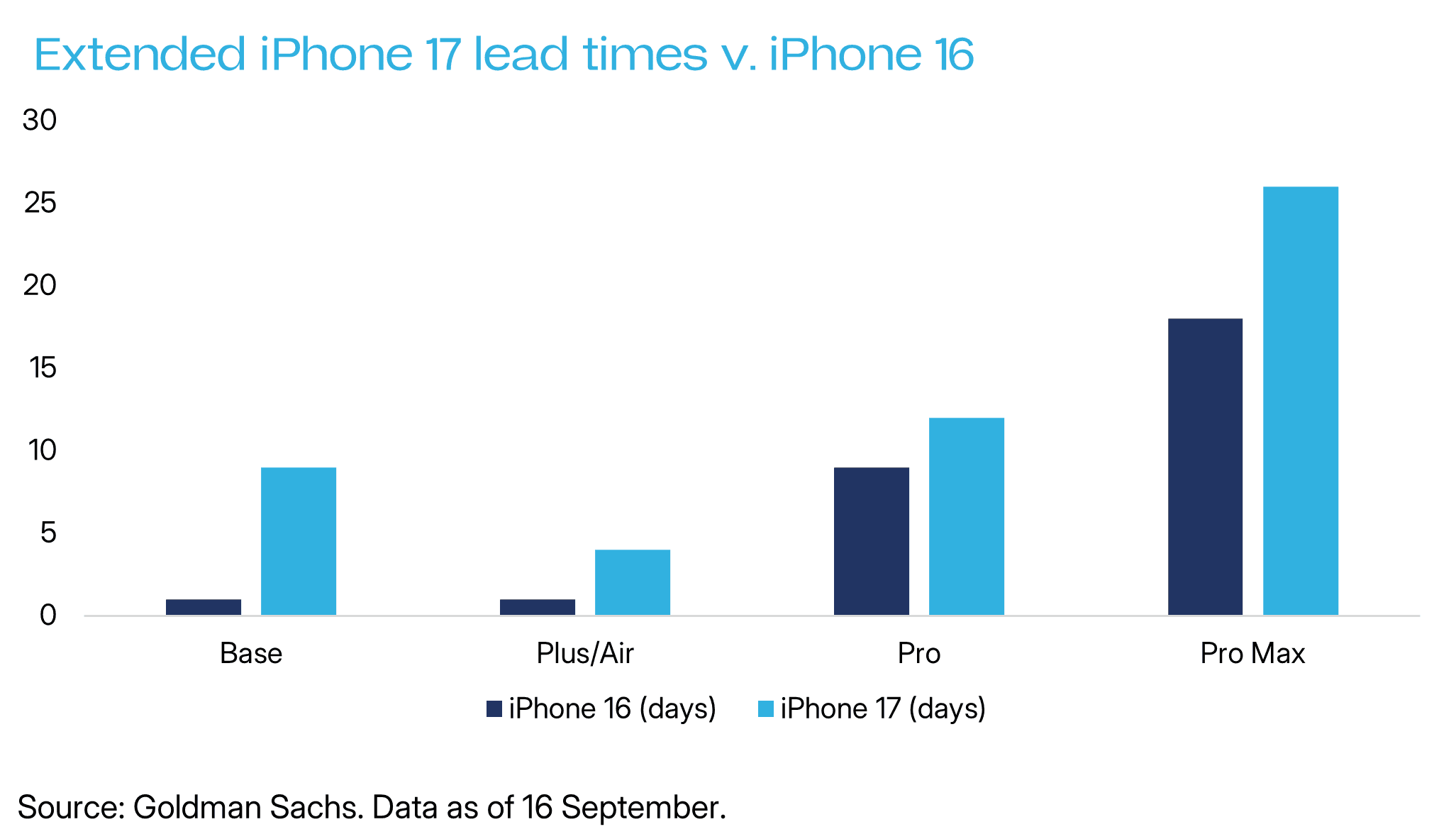

Then came the iPhone 17.

Cook reads customer emails every morning. He read the complaints about the iPhone 16’s low battery life and overheating. The iPhone 17 dealt with the complaints head on.

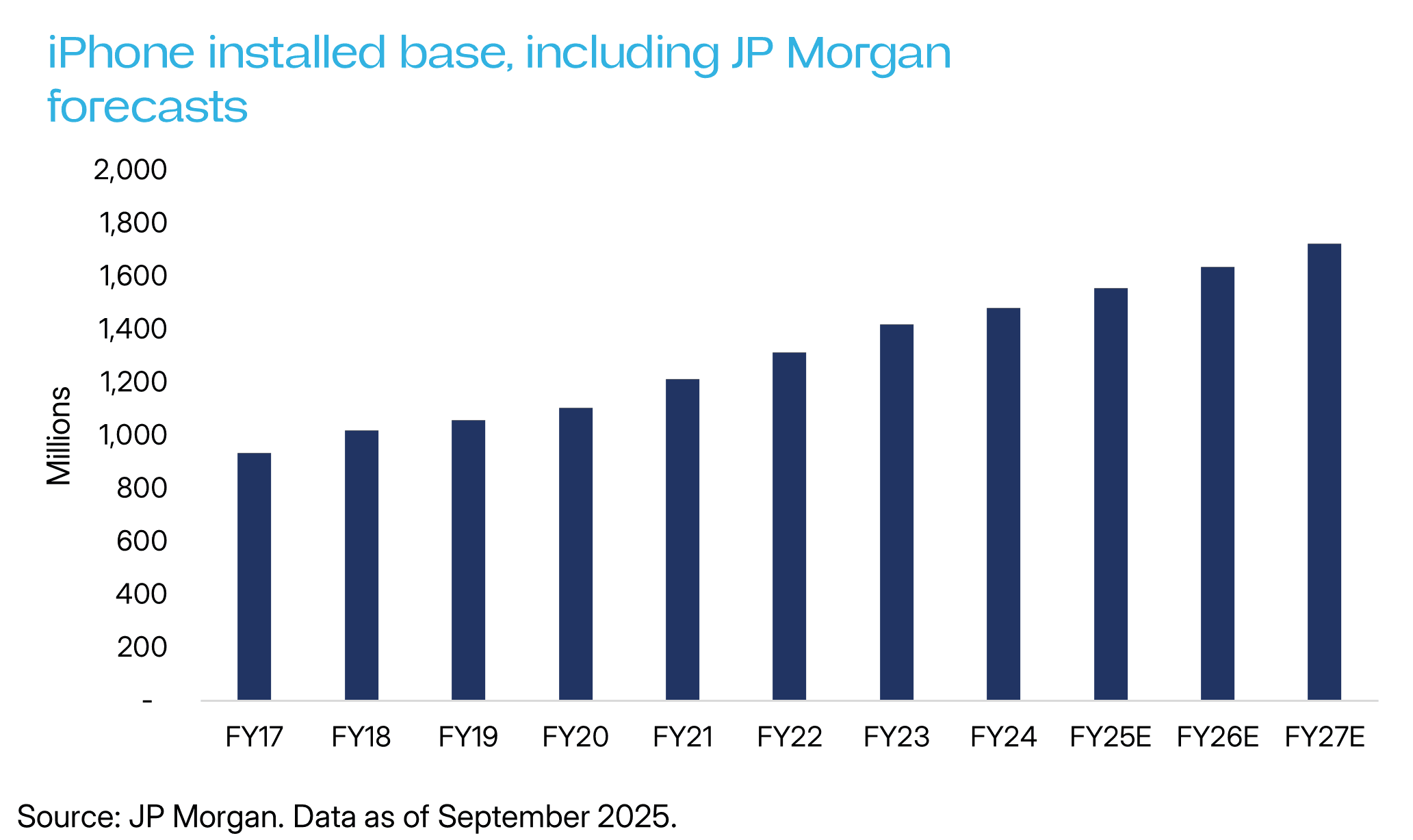

The result: iPhone 17 is selling above expectations, forcing Wall Street to lift revenue and profit forecasts. But the real story is its expansion of Apple’s “installed base” – the hundreds of millions of active Apple users who are the bedrock of its services strategy.

Services: Apple’s growth arc

If the iPhone 17 is the door, services are the castle inside.

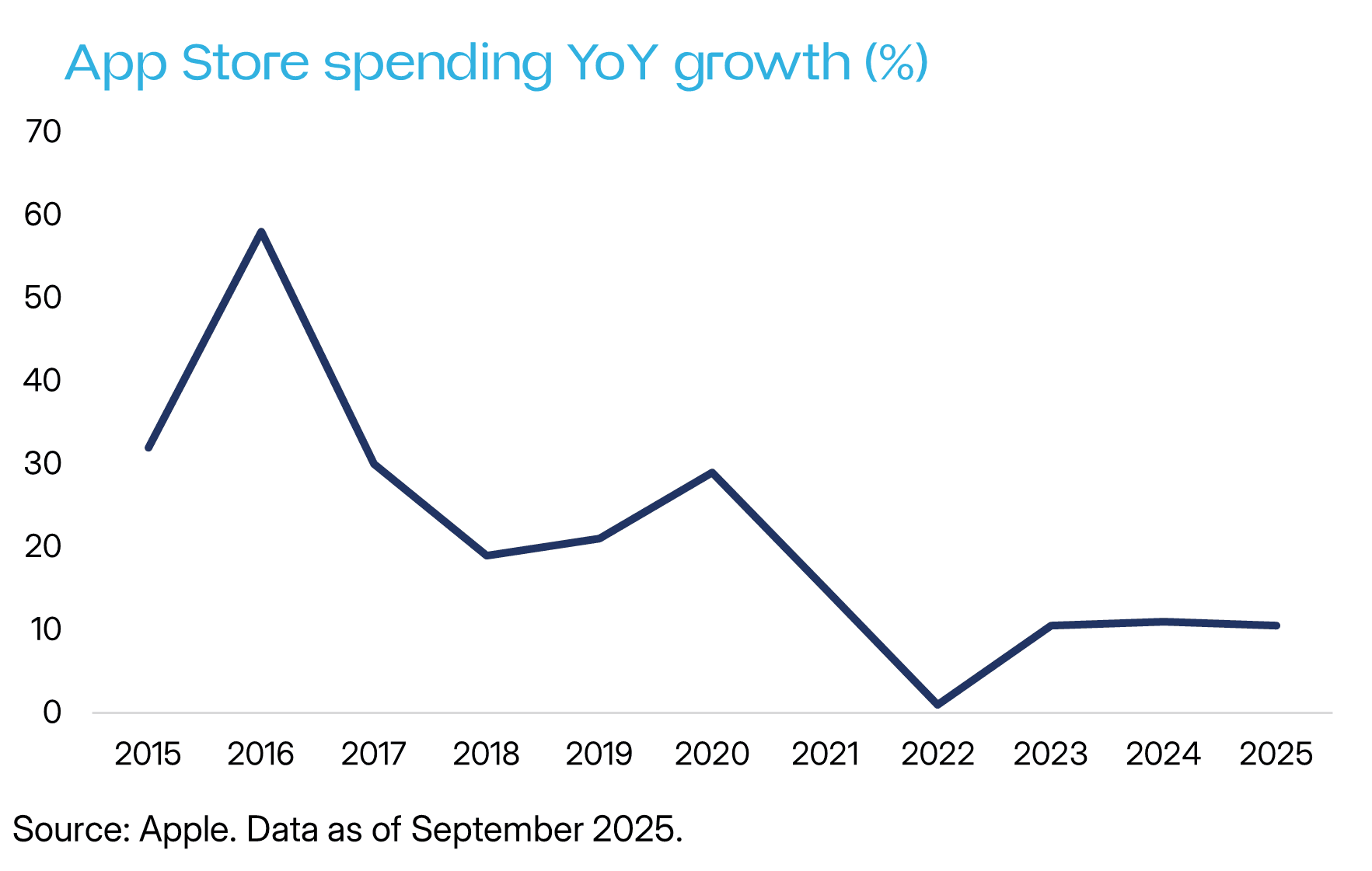

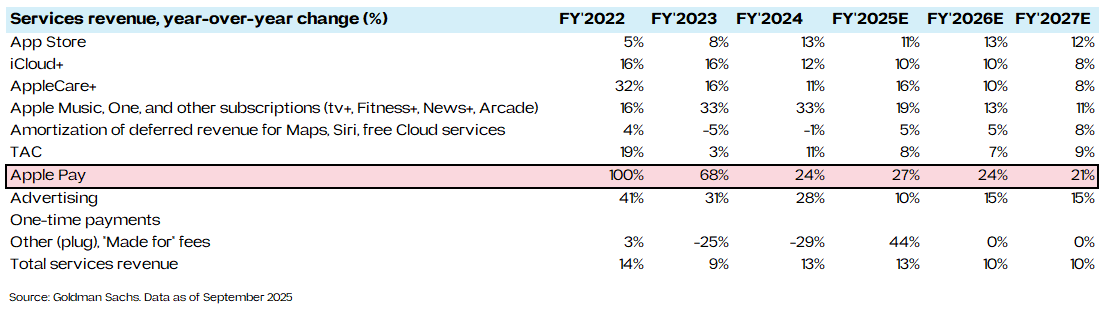

Services generate gross margins of about 70% for Apple, roughly double the 35% on iPhones. And with the latest numbers showing services revenue growth of nearly 10% last quarter, the trajectory looks strong.

Apple’s services are varied.

Some – Apple TV+ or iCloud – are loss leaders that keep customers tied to the ecosystem.

Others – App Store, Apple Music, Apple Pay – are profit engines.

The App Store remains the crown jewel. And within it, Apple’s grip on video games. As gaming migrates away from consoles and onto iPhones, Apple is emerging as its de facto landlord.

Key sensitivities for Wall Street though are Apple Pay and Apple Music. Apple Pay is making PayPal struggle. It is Apple’s fastest-growing service, and as payments shift onto the iPhone, its growth runway looks effectively limitless. Apple Music is gaining ground on Spotify in the US, as it offers artists bigger royalties and consumers lower prices.

Optionality: MedTech and Metaverse

Where Apple still looks cheap is in its optionality on future tech, particularly the metaverse and medtech.

In September, the Apple Watch quietly won FDA approvals for health features. It is seeking them for blood pressure monitoring, a leap that could turn it from a fitness accessory into a genuine medical device. If Apple makes the Watch as medically indispensable as the iPhone is socially indispensable, it unlocks another adoption wave.

Then there’s the metaverse. Everyone laughed off Zuckerberg’s pivot in 2022. But Apple didn’t. The metaverse has genuine traction in engineering, architecture and construction. It is one of those rare themes – like AI – with US military backing. Cook himself is betting his legacy on it. If Vision Pro sales keep growing, Apple could spin up a new hardware-plus-services flywheel that Wall Street hasn’t even begun to price in.

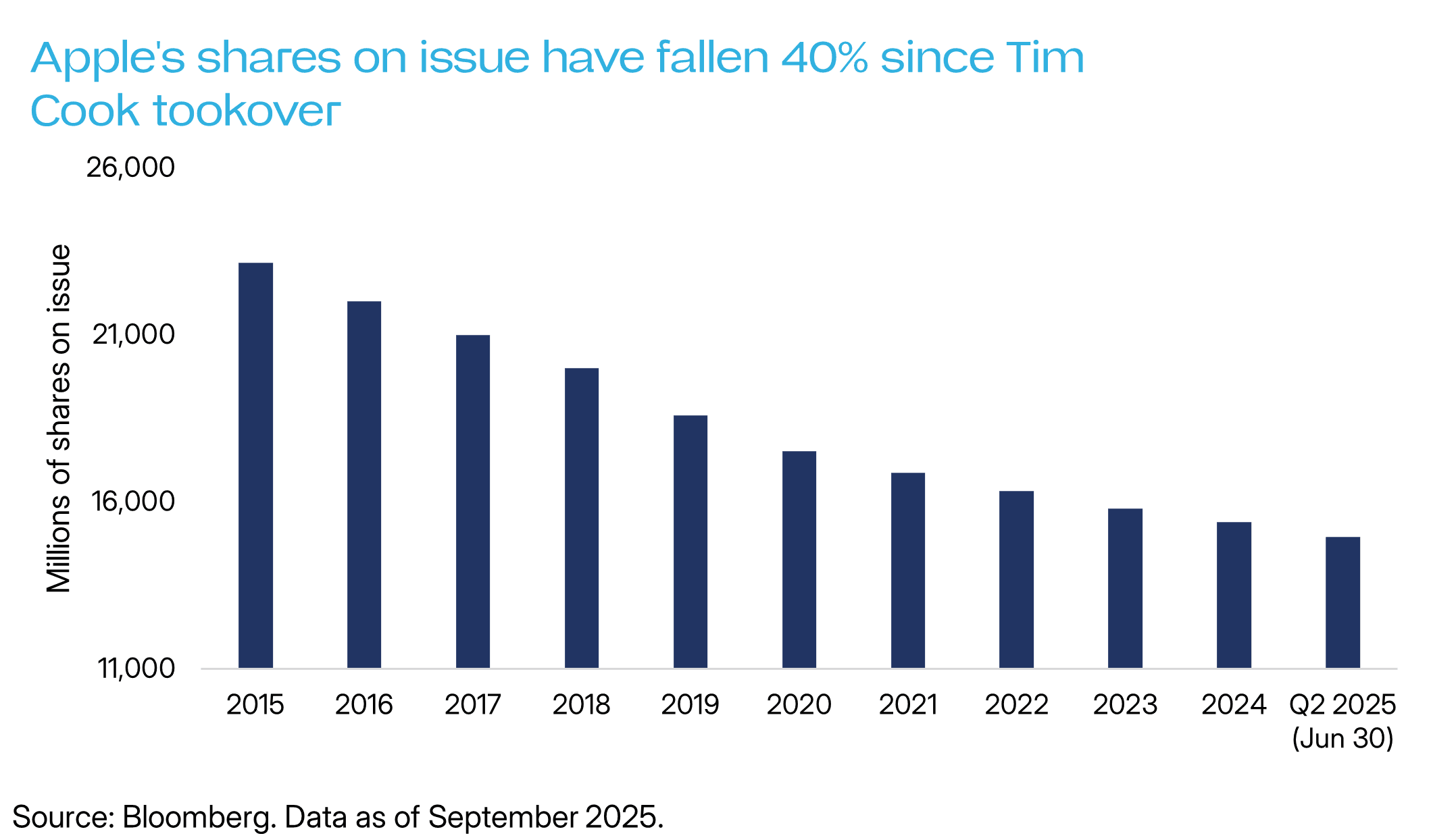

Buybacks and the infinite share price

Since 2012, Apple has been quietly running what amounts to a leveraged buyout of itself. More than 40% of shares have been retired. The impact is profound: non-committal investors are steadily removed, leaving a loyal base of retail holders that rarely sells.

The result is a share register with almost no natural supply. Overlay an endless bid from Apple itself, and the logic follows: the share price of a company that keeps shrinking its share count while shareholders refuse to sell is, in theory, infinite.

Disclaimer

ETF Shares Management Limited ABN 77 680 639 963, AFSL: 562766. Investing involves risk and returns are not guaranteed. Before investing, you should consider seeking independent advice and read the relevant PDS and TMD available at www.etfshares.com.au.