Summary:

- Evidence suggests Musk's political involvement has harmed Tesla's bottom line.

- Meanwhile Tesla is also struggling with increased competition from BYD.

- However the long-term bull case for Tesla looks bright, especially given its place in robotaxis.

Tesla has taken a hit

This fortnight – for the first time in a year – Elon Musk has stayed out of the news.

Musk staying quiet – and out of politics – is a positive development for shareholders and is being welcomed by his supporters like Cathie Wood.

Since Musk became more political, Tesla has taken a hit. This shows in several places.

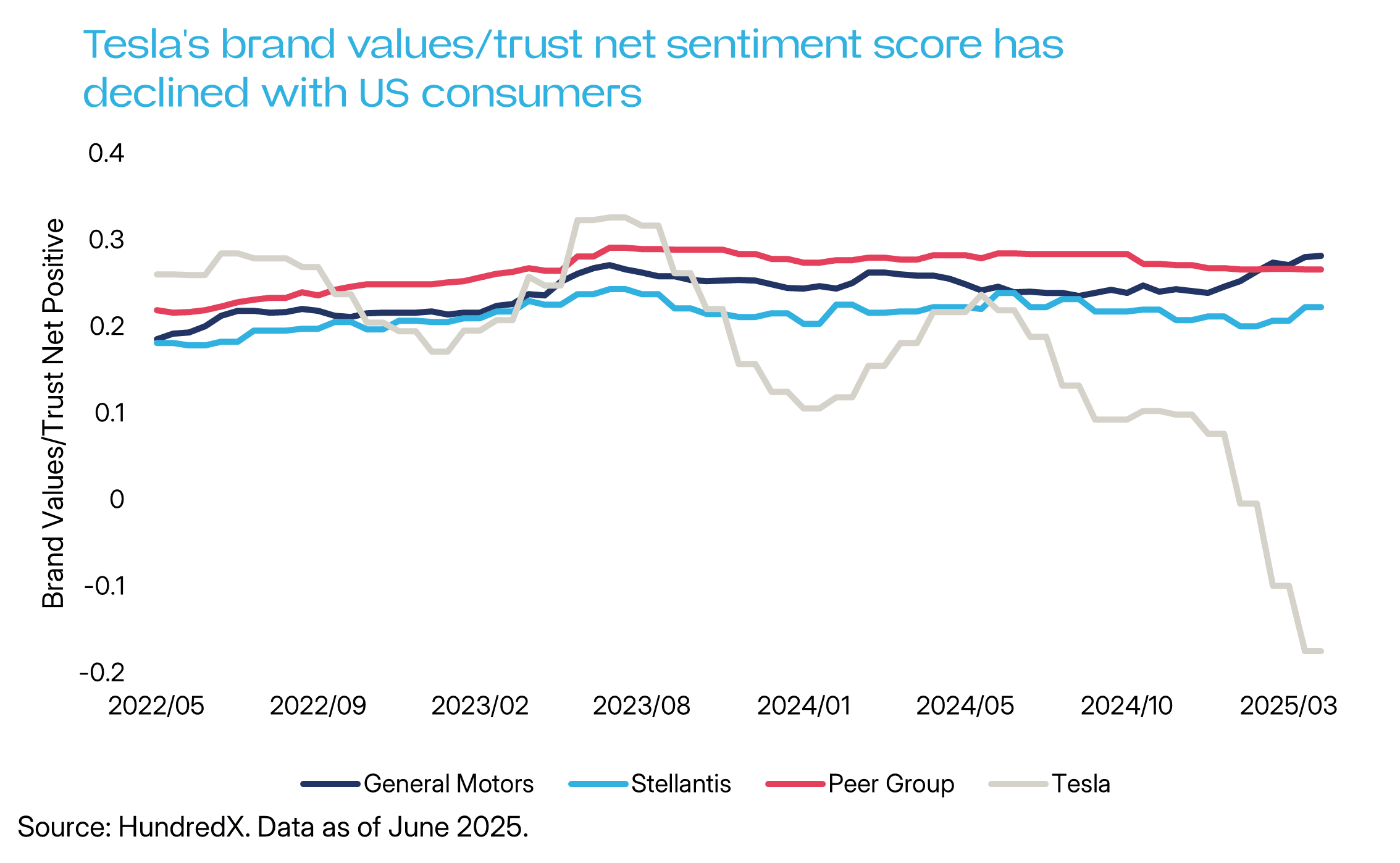

Public perceptions, always important for consumer-facing companies like Tesla, have declined. This is reflected in lower brand value perceptions among consumers, per the chart below.

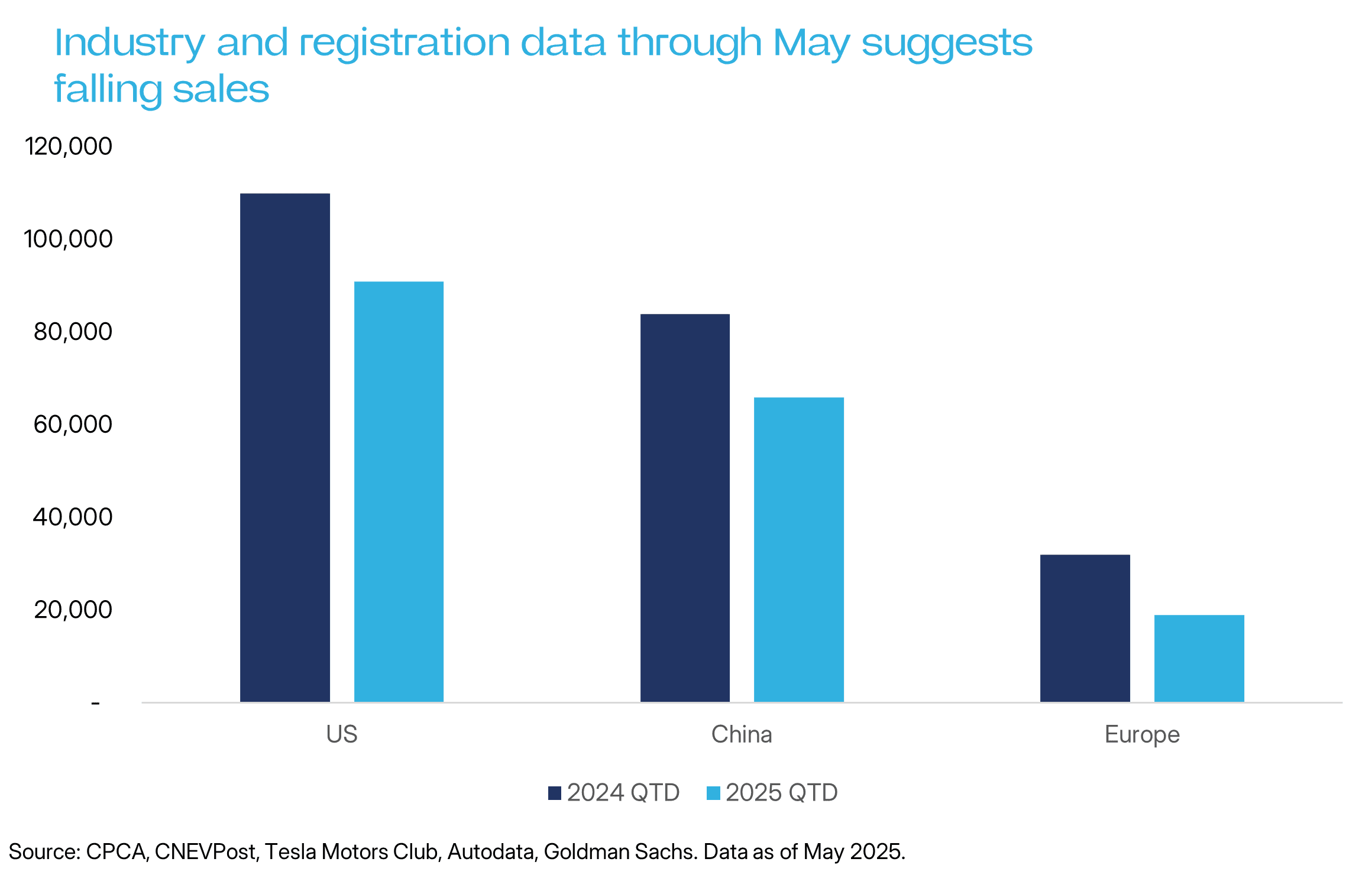

Declining brand perceptions have translated directly into falling sales. In all three major markets - US, China and Europe – Tesla sales are down this quarter compared to Q2 in 2024. These declines have occurred despite electric car sales rising overall—particularly in Europe.

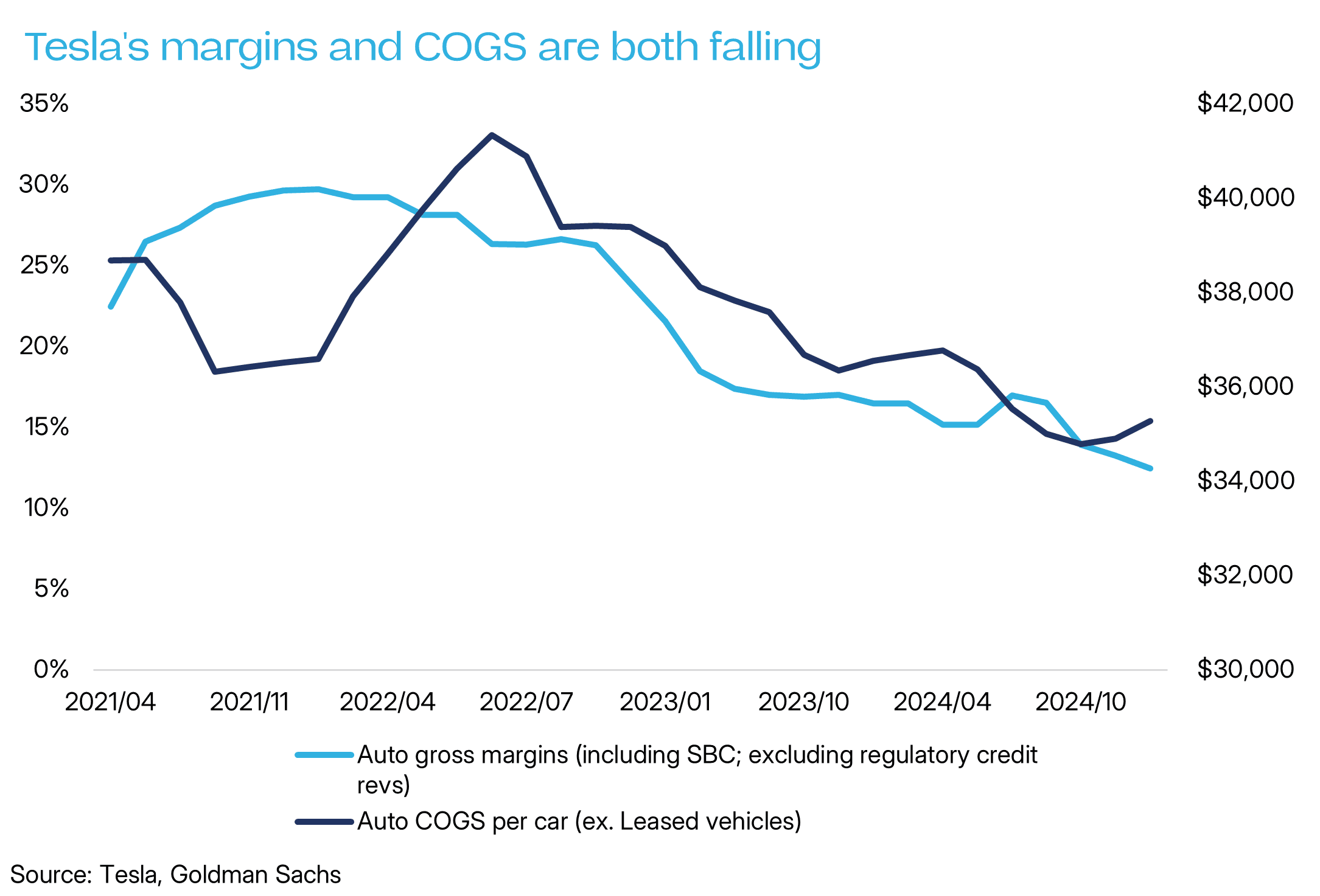

This compounds existing difficulties for Tesla that are unrelated to politics. Crucially, Tesla is under sustained pressure from BYD, China’s national electric car champion both in China and in Europe.

A key competitive edge for electric car makers is where they sit on the battery cost curve. Batteries are the biggest cost of making an electric car. Car companies that producer cheaper batteries therefore produce cheaper cars—a structural advantage.

Here, BYD has widened the gap between itself and Tesla in recent years—sitting increasingly lower on the battery cost curve. And able to aggressively underprice Tesla. This has forced Tesla to reactively cut prices and shrink its margins. This is reflected in the chart below.

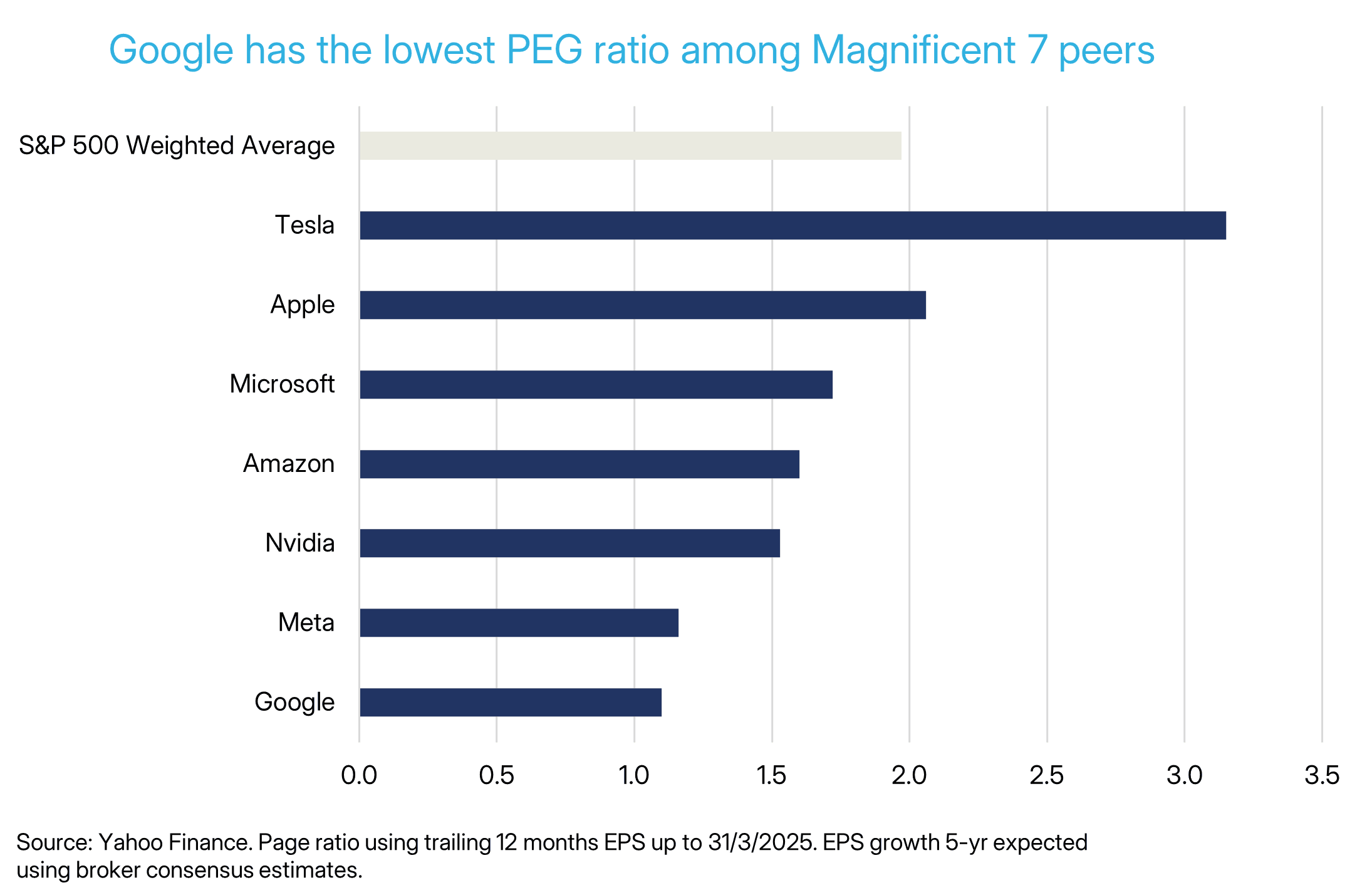

These difficulties have all meant that Tesla has been the worst-performing Magnificent 7 stock this year. And thanks to growth estimates falling, its valuation – as measured by the PEG ratio, our preferred measure – also looks the most stretched among its magnificent 7 peers.

Tesla’s bull thesis remains strong

Musk staying quiet allows investors to focus on Tesla’s fundamentals and long-term investment thesis once more. Here, there is a lot to like.

Viewed in revenue terms, Tesla is fundamentally a car company. In 2024, 90% of revenue came from car sales. But given how deeply Tesla invests in futuristic technology – self-driving cars, AI, robotics, and energy storage – it is often trades more like a long-dated call option on megatrends.

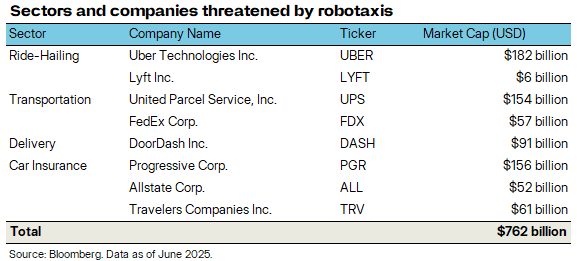

Self-driving cars and robotaxis are what has the market most excited. Musk himself believes they are central to Tesla’s future. It is easy to see why. Musk is trying to build self-driving cars in a much cheaper way than its top competitor, Google-owned Waymo. If this promise is realised, Tesla’s robotaxis could disrupt several industries simultaneously: taxis, ride-hailing apps, logistics, delivery, and car insurance. (Tesla is an insurer).

Currently, major US-listed companies providing these services have more than US$760 billion in combined market capitalisation. This figure rises further when global companies are included. This value could, in theory, could shift towards Tesla if it successfully delivers self-driving cars, robotaxis and a supporting app.

Notably, Tesla’s robotaxis and self-driving cars would be software-based, enabling recurring, high-margin revenue, a departure from traditional capital- and labour-intensive models.

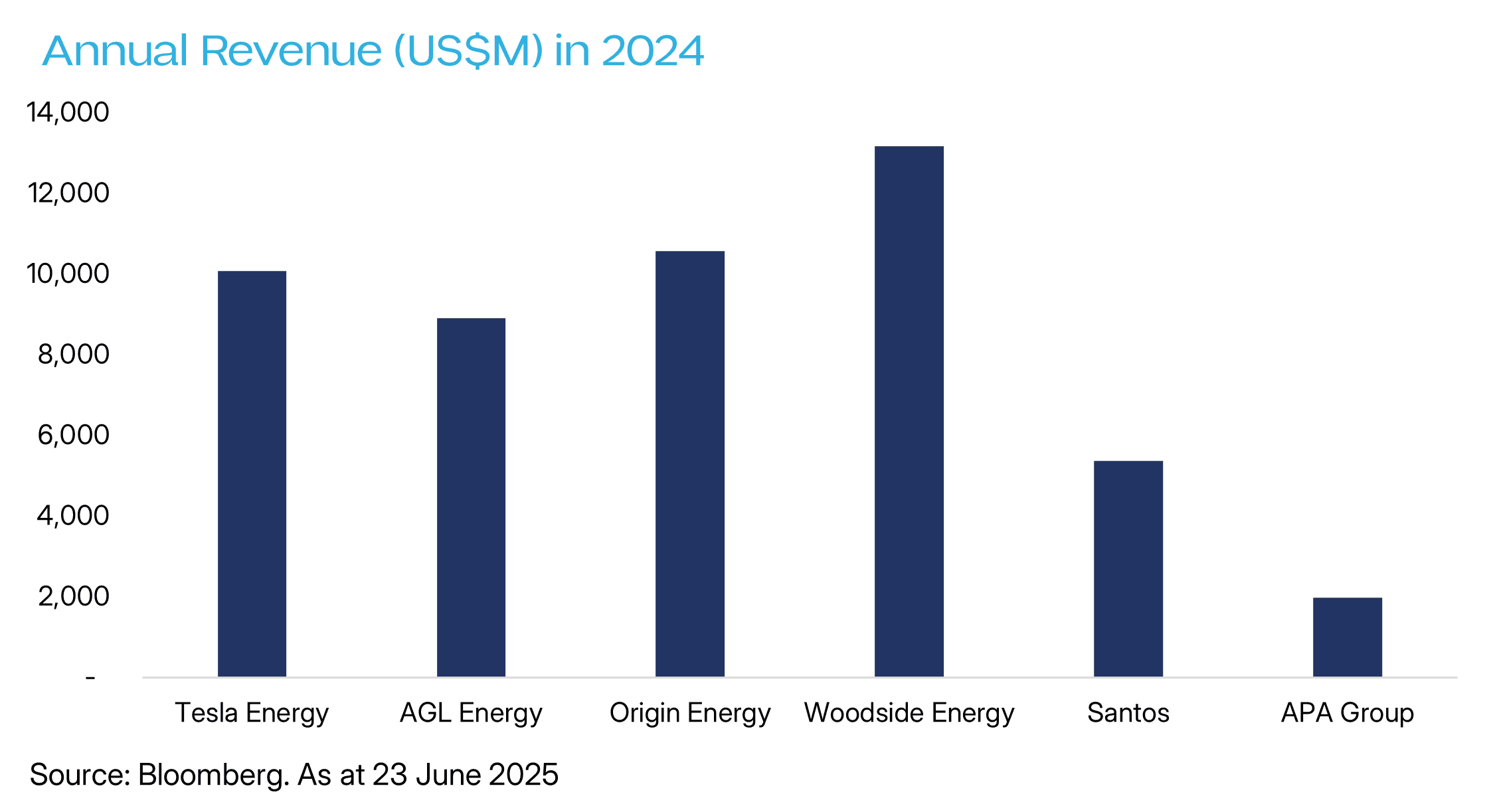

Tesla Energy — its fastest-growing and highest-margin division in Q1 2025 — remains an overlooked bright spot. In 2024, it quietly overtook Australia's largest listed energy companies by annual revenue. However analysts expect Tesla Energy’s revenue to taper off in 2025 as Trump removes Joe Biden’s green energy subsidies.

Still, Tesla Energy has a formidable moat. Its software (e.g. Autobidder, Powerhub) give it a clear edge in optimising storage, trading, and load balancing. Something traditional utilities don’t really do.

Financially, Tesla is unusually robust for a company with so many speculative growth levers. It generates positive free cash flow, carries little debt, and sits on a lot of cash. That mix — scale, ambition, and financial discipline — is rare, perhaps unique, and undergirds why investors see and treat Tesla differently.

Related ETFs

For those wanting to invest in Tesla, the ETFS Magnificent 7+ ETF (HUGE) takes one of the most concentrated bets on the firm of any ETF in Australia. The Fund gives investors exposure to the largest 10 US companies on the NASDAQ Stock Exchange.

Disclaimer:

The issuer of units in ETFS Magnificent 7+ ETF (HUGE) (ARSN: 685 356 183) is the responsible entity of the Fund, being ETF Shares Management Limited (AFSL: 562 766). The product disclosure statement (PDS) for the Fund contains all of the details of the offer of units in the Fund. Copies of the PDS are available from ETF Shares Management Limited or at www.etfshares.com.au. In respect of each retail product, ETFS has prepared a target market determination (TMD) which describes the type of customers who the relevant retail product is likely to be appropriate for. The TMD also specifies distribution conditions and restrictions that will help ensure the relevant product is likely to reach customers in the target market. Each TMD is available at www.etfshares.com.au

The information provided in this document is general in nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information in this document, you should consider the appropriateness of the information having regard to your objectives, financial situation or needs and consider seeking independent financial, legal, tax and other relevant advice having regard to your particular circumstances. Any investment decision should only be made after obtaining and considering the relevant PDS and TMD.

Investments in any product issued by ETFS are subject to investment risk, including possible delays in repayment and loss of income and principal invested. None of ETFS, the group of companies, or their respective directors, employees or agents guarantees the performance of any products issued by ETFS or the repayment of capital or any particular rate of return therefrom.

Solactive AG (“Solactive”) is the licensor of Solactive Magnificent 7+ Index (the “Index”). The financial instruments that are based on the Index are not sponsored, endorsed, promoted or sold by Solactive in any way and Solactive makes no express or implied representation, guarantee or assurance with regard to: (a) the advisability in investing in the financial instruments; (b) the quality, accuracy and/or completeness of the Index; and/or (c) the results obtained or to be obtained by any person or entity from the use of the Index. Solactive does not guarantee the accuracy and/or the completeness of the Index and shall not have any liability for any errors or omissions with respect thereto. Notwithstanding Solactive’s obligations to its licensees, Solactive reserves the right to change the methods of calculation or publication with respect to the Index and Solactive shall not be liable for any miscalculation of or any incorrect, delayed or interrupted publication with respect to the Index. Solactive shall not be liable for any damages, including, without limitation, any loss of profits or business, or any special, incidental, punitive, indirect or consequential damages suffered or incurred as a result of the use (or inability to use) of the Index.

The value or return of an investment will fluctuate and an investor may lose some or all of their investment. Past performance is not a reliable indicator of future performance.