The price of gold has breached a key resistance level, sparking surging trading volumes.

The rally is being driven by a familiar story: Trump’s campaign against the Fed and the US dollar.

But from where we sit, the economics of this gold rally suggest investors should be taking profits. And the gold bull thesis, in our view, looks like a political bet on China.

US dollar giveth, Aussie dollar taketh away

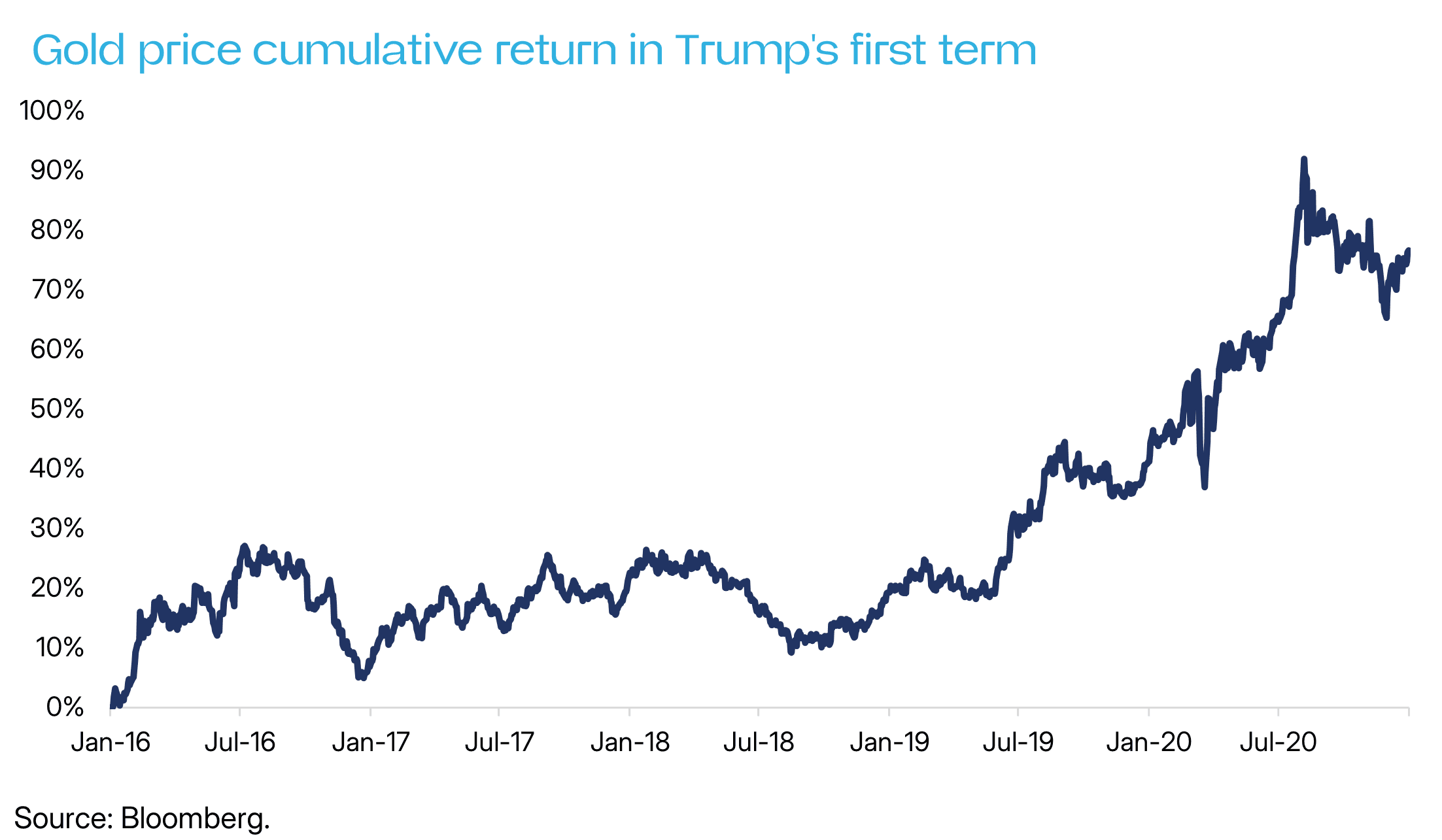

Between 2016 and 2020, gold climbed as Trump demanded rate cuts and a weaker dollar. Today’s rally is a direct bet on a sequel.

That Trump wants a weaker dollar is no secret. “You make a hell of a lot more money with a weaker dollar,” he recently told reporters. “When you have a strong dollar, you can’t sell anything.”

His team is already applying pressure.

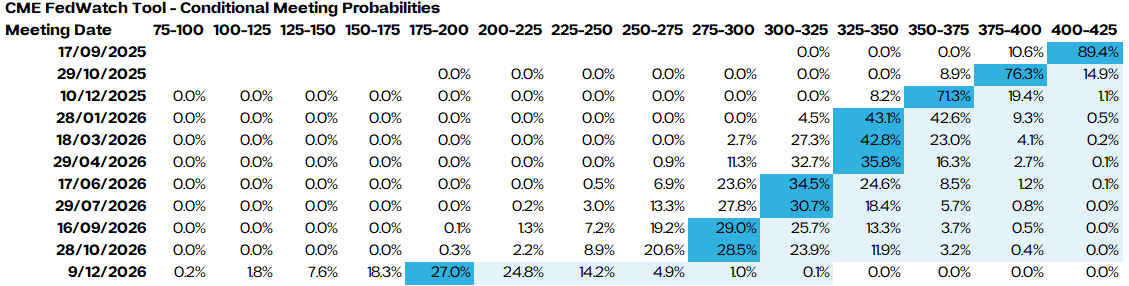

US treasury secretary Scott Bessent has publicly called for 125 - 150 basis points of rate cuts. Markets have already priced much of this into futures, as in the graph above.

But the real excitement for gold comes from targets floated by Trump himself: a funds rate around 1% by early 2026. That would imply roughly 300 basis points of cuts within six months, a massive catalyst that has not yet been fully priced into Treasury or currency markets.

Trump has a record of surprising investors by sticking to his word. Over the past 12 months, bets on him simply doing what he says he will do - privatise Fannie Mae cuts to clean energy funding - have paid off handsomely.

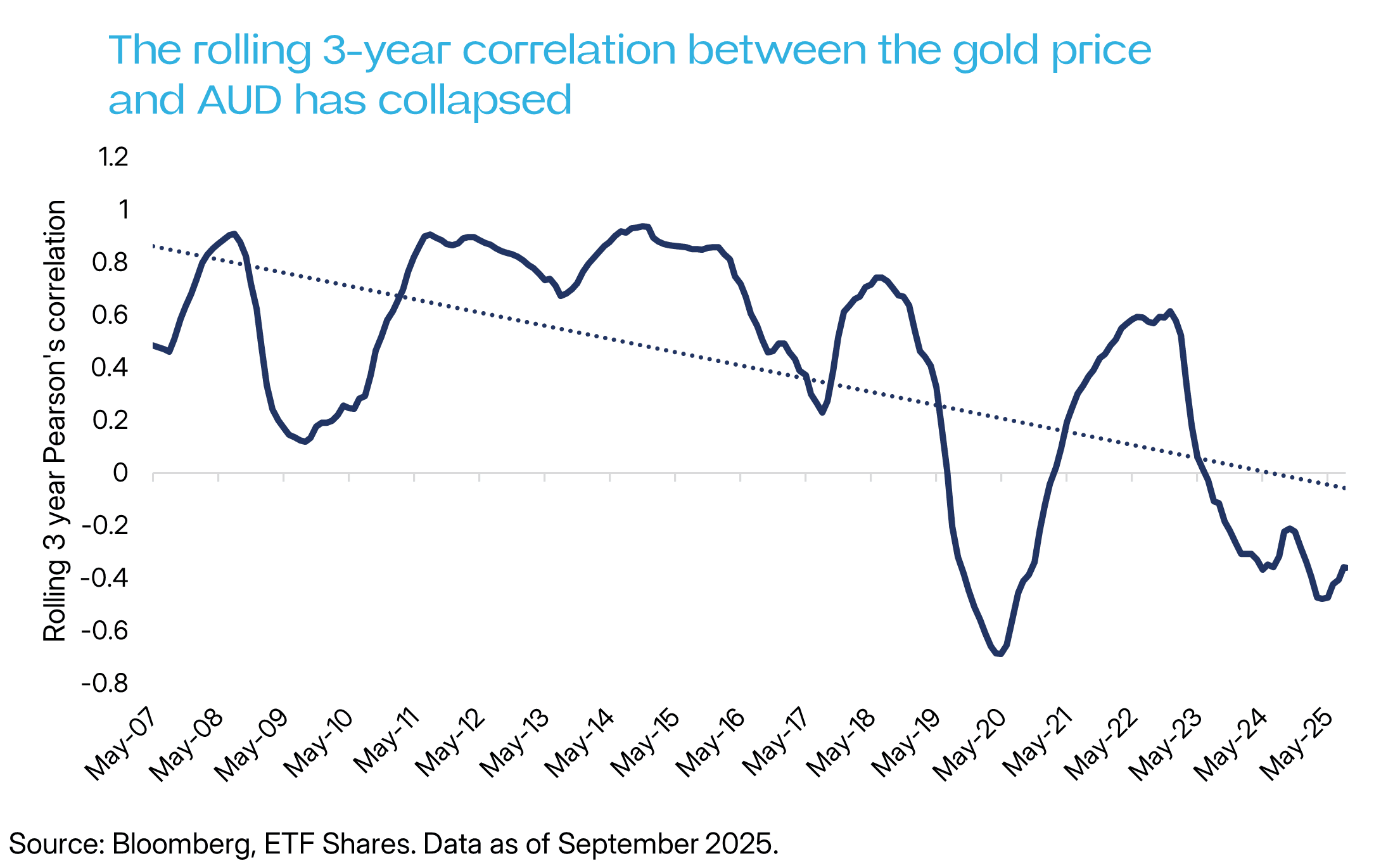

However, for Australian gold investors, any win may be pyrrhic. A weaker greenback can propel the gold price higher in USD terms, but it also tends to lift the Australian dollar. And the gold price, officially quoted in USD, translates back into fewer Aussie dollars.

This is not a trivial detail. The rolling 3-year correlation between gold and AUD/USD was 0.85 in July 2015, meaning the Aussie dollar and gold reliable rose together. But by July 2025, the correlation had flipped to -0.36, meaning the Aussie dollar and the gold price these days tend to go in opposite directions.

For an unhedged Australian investor, buying gold is therefore a double bet: gold must rise enough in USD terms to outweigh a rising local currency. A simple illustration: if gold gains 10% but the AUD strengthens 7% against the USD, the net return to an Aussie investor is only 3%. And the correlation data above suggests the Aussie dollar and gold price are increasingly unlikely to rise simultaneously.

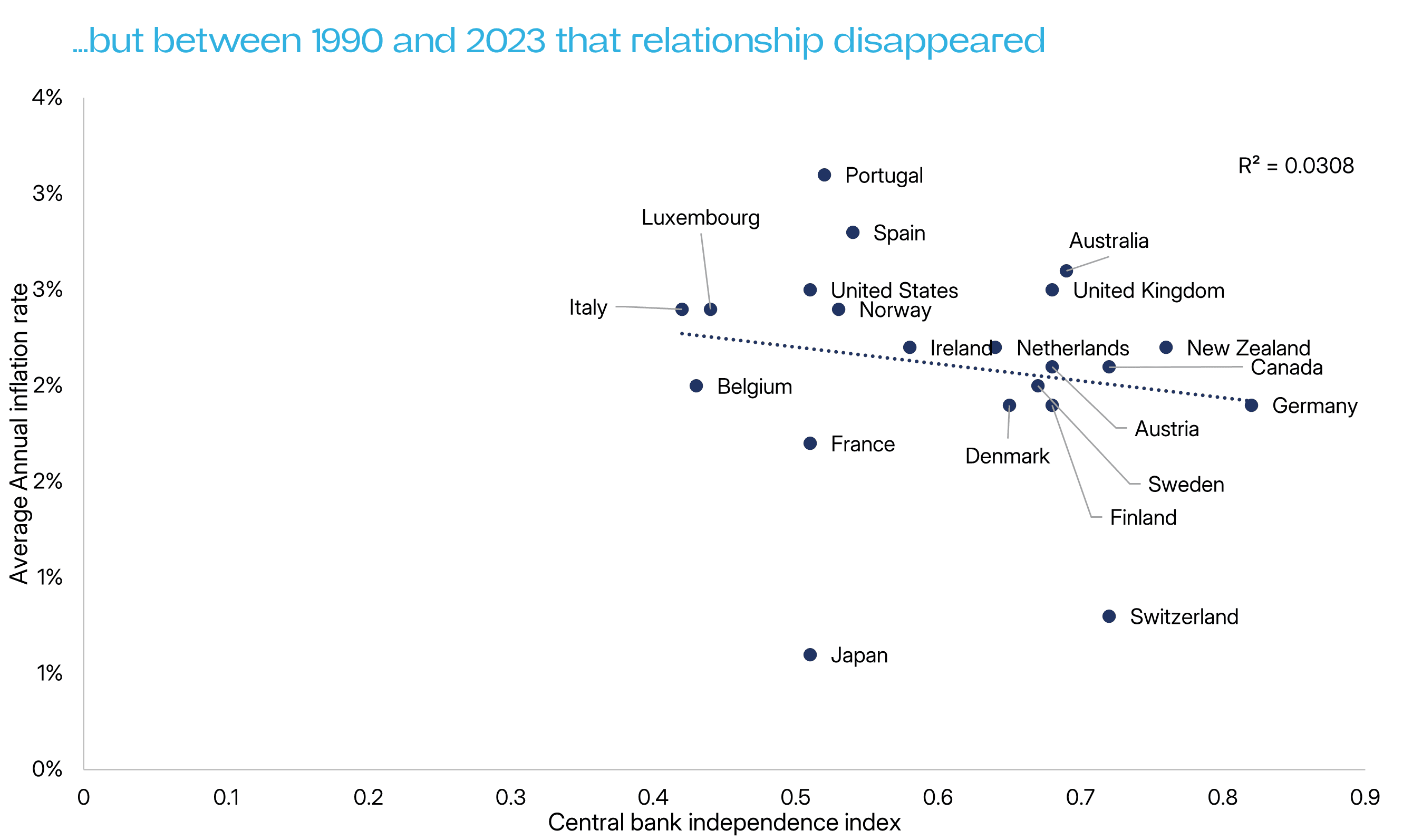

The independent central bank fallacy

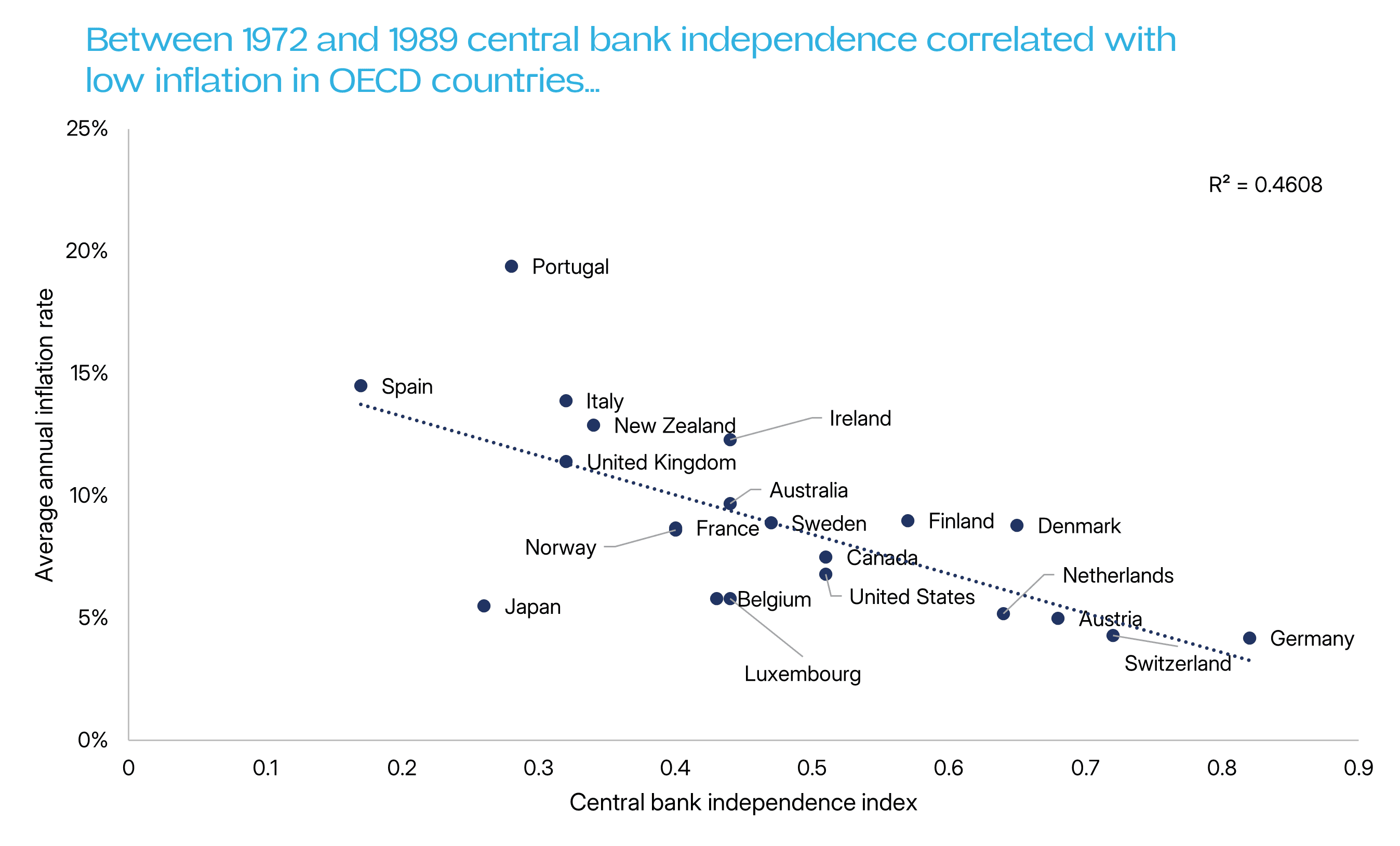

The second pillar of the bull case for gold rests on fears of resurgent inflation. The argument goes that a Fed stripped of independence will print money, debase the currency, and lift gold.

This logic is rooted in the 1970s stagflation crisis, after which central bank independence became sacrosanct. Seminal research at the time showed a strong negative correlation between a central bank’s independence and inflation rates.

But that was then. More recent studies - including a 2021 BIS survey - show this relationship has broken down. In today’s global economy, central bank independence is no longer a reliable predictor of inflation. The historical data that once justified the thesis no longer holds, meaning a politically influenced Fed may not be the inflation catalyst gold bulls expect.

But if China is buying, does any of it matter?

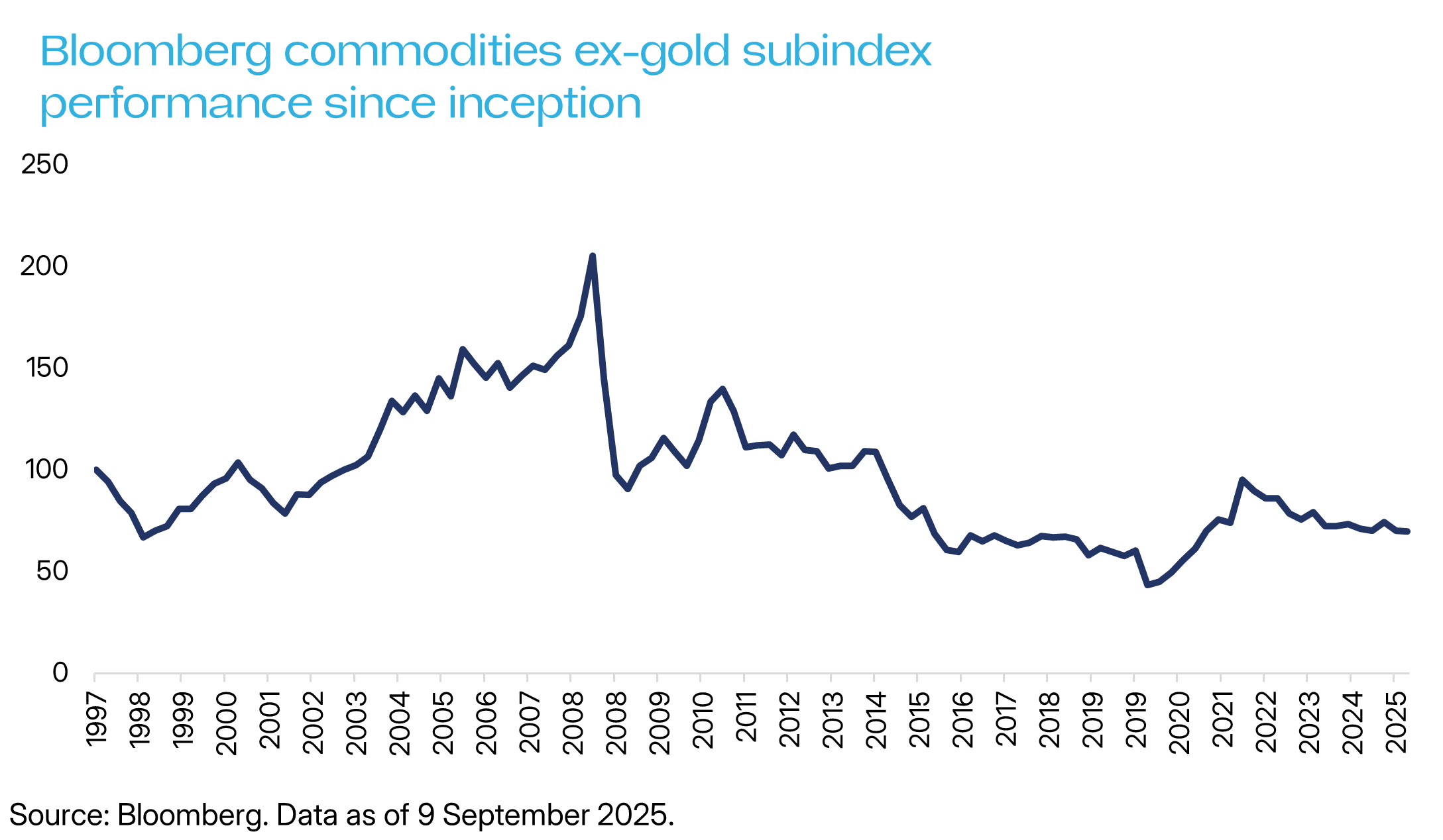

Commodities usually make poor investments. When you buy food, energy, or building materials, governments are actively working to push prices down. They use every lever available - subsidies, regulation, stockpiling - to suppress costs for households and businesses.

Gold is different. Governments themselves, through central banks, are long gold. The effect of this shows up in the data: if you strip gold out of the Bloomberg Commodities Index, there has been no sustained breakout in commodity prices in 30 years.

So today’s gold price largely hinges on one question: what will governments do? If China, Russia and India continue accumulating regardless of inflation, then a bull case exists. But even then, any local-currency appreciation could offset much of the gain. For Australians especially, that leaves a complicated, fragile thesis - more political bet than safe haven.

That’s not to say it’s wrong: but only to say that investors should go in with open eyes.

Disclaimer

ETF Shares Management Limited ABN 77 680 639 963, AFSL: 562766. Investing involves risk and returns are not guaranteed. Before investing, you should consider seeking independent advice and read the relevant PDS and TMD available at www.etfshares.com.au