Everything gets called a bubble these days.

Last month it was AI. This month its gold.

Neither is a bubble. The gold rally, for its part, is being driven by a flood of money exiting US dollar assets – particularly treasuries – and going into gold.

The relationship between US treasuries and gold is kind of like the sun and the earth. The sun (treasuries) is much larger than the earth (gold). The earth orbits the sun. And tiny changes in the sun – like solar flares, let’s say – can cause massive changes on earth.

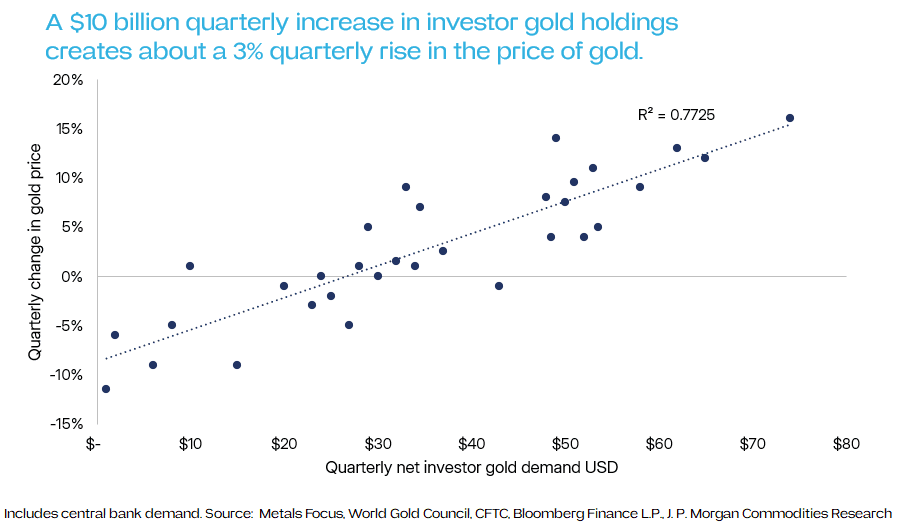

JP Morgan recently quantified this relationship. On their numbers, a mere 0.1% shift out of US treasuries and into gold – the solar flare – is enough to drive the gold price 18% higher. This is reflected in the graph above.

A rotation of this kind has been occurring this year. If it continues this quarter, gold will punch above US$5,000/oz with ease before Christmas. And this is before momentum traders and other bandwagoners add fuel to the fire.

Beijing has written a put option on gold

At the heart of this switch from US dollar assets to gold are escalating US-China tensions. It’s for this reason we saw the gold price drop 2% on Friday as Trump and Xi deescalated trade tensions.

Since China joined the WTO, the quality of life for many working-class Americans has declined as Chinese exporters have hollowed out the US manufacturing base. Rather than address the domestic policy failures that allowed this, Washington has found it politically convenient to blame Beijing.

China has responded by sketching out an alternative to the US dollar fiat system, underpinned in part by gold.

China has worked with other BRICS countries to try and create a yuan and gold backed currency system. Meanwhile at home, state messaging is driving record demand among Chinese investors.

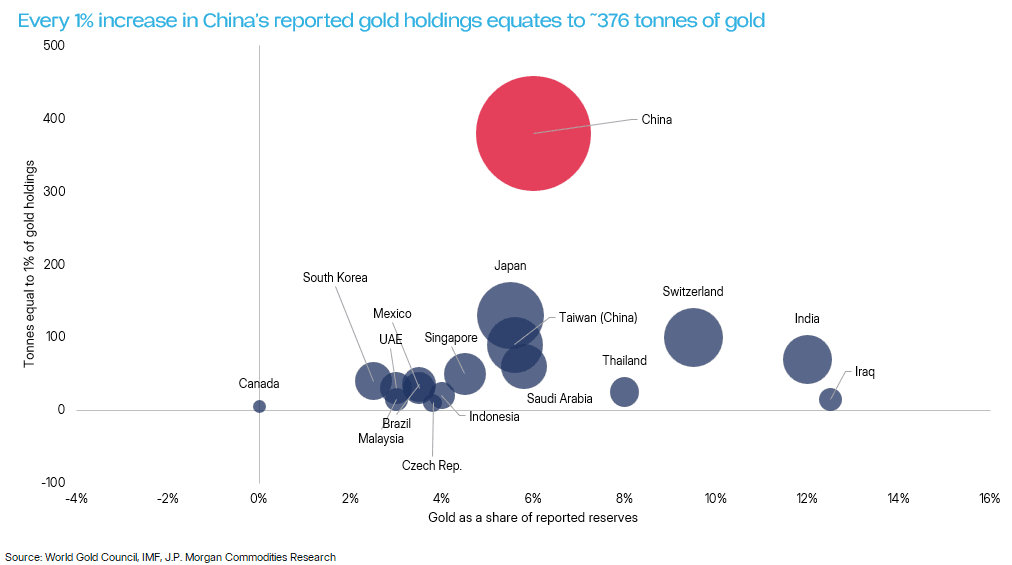

The People’s Bank of China has been buying gold in record quantities since 2022, often buying the dip. Again, to quantify things: on JP Morgan’s numbers a 1% increase in PBoC’s gold holdings in a given quarter can, all else being equal, drive an almost 8% rally in the gold price.

The net effect is a gold market that is now less risky, as the weight of the world’s second most powerful state backstops it.

Fundamentals: Inelastic supply meets surging demand

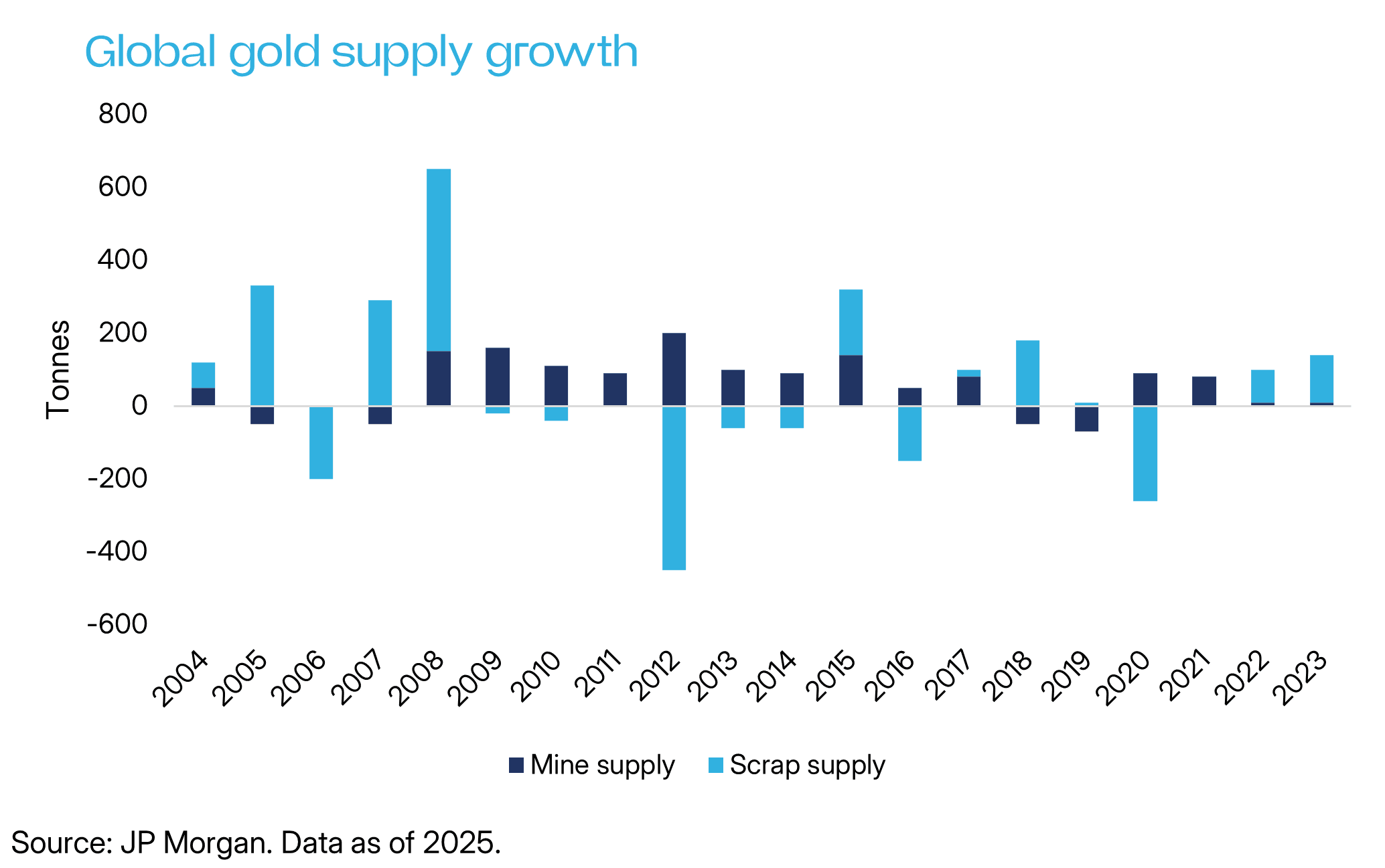

This demand shock is hitting a small market where supply simply cannot keep up.

Roughly 200,000 tonnes of gold have been mined in human history. Nearly all of this still exists as above ground supply, as gold is chemically inert. Yet new production has barely grown since 2018 – and supply growth remain flat at around 1.5% new gold per year.

Gold miners want to capitalise on high prices. But they are grappling with declining ore grades, rising costs, and stricter environmental regulations.

Recycled gold offers some supply uplift. But even with higher prices, the growth in total available gold has been modest.

There is huge investment going into gold miners and explorers right now. But it will take several years – possibly a decade – for this to translate into major supply. By this time the gold price will be somewhere else.

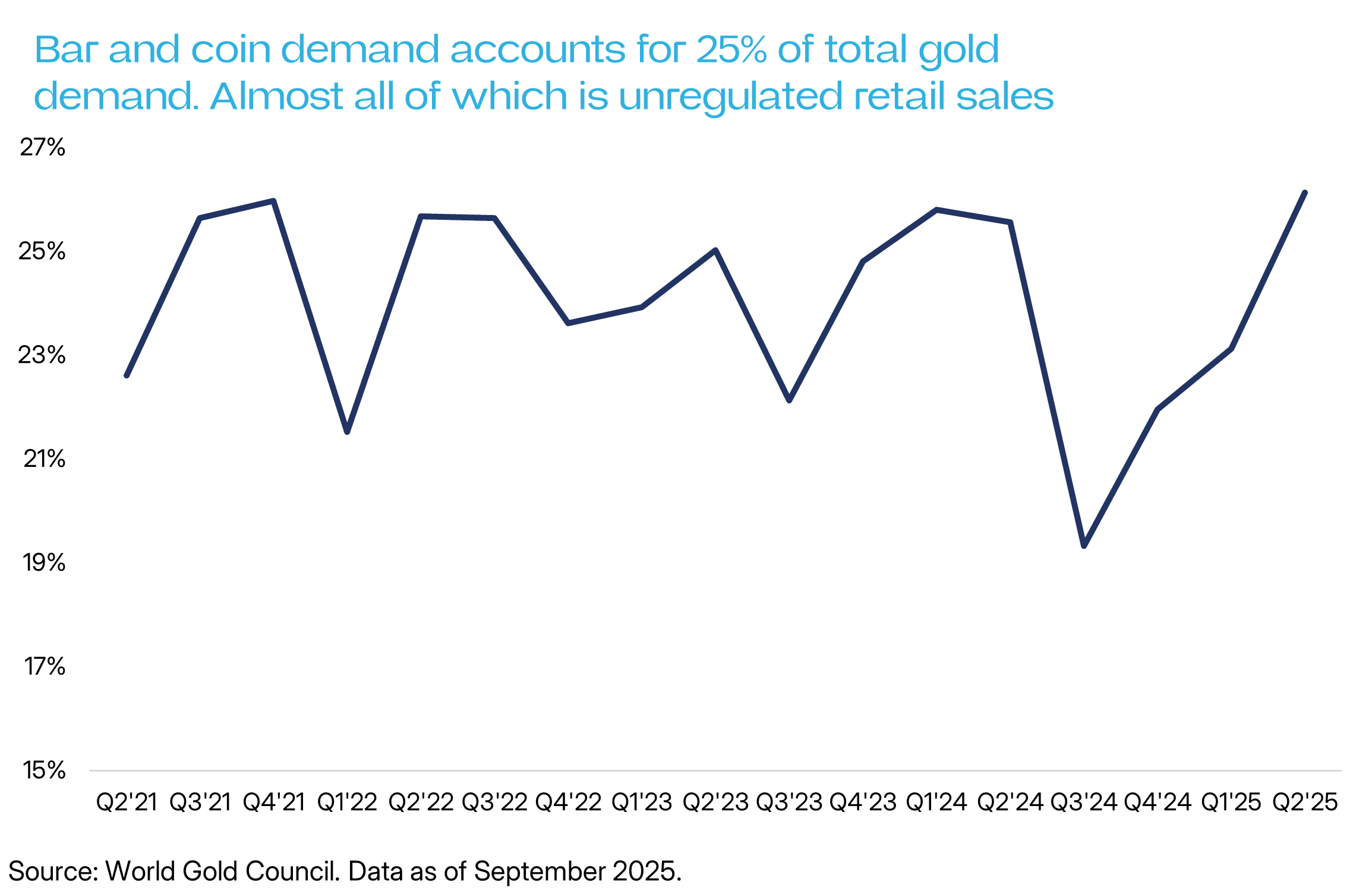

The one caveat: Unregulated retail herding

While gold is not a bubble, there is a lot of retail investor herding around gold coins and bars. This has – justifiably – drawn a lot of commentary on LinkedIn.

Why the concerned commentary is justified: selling gold bars and coins to retail investors is essentially unregulated – in Australia as elsewhere. Gold bars and coins can be marketed and sold directly to mums and dads in a way that shares, bonds and even gold ETFs cannot be.

This matters because retail sales have been the primary transmission mechanism for bubbles this century. (Although not the only one: lithium’s bubble in 2021 had little to do with retail). And retail punters buying bars and coins makes up roughly a quarter of all gold demand.

The evidence suggests this engine is now starting to fire in the physical gold market. Where it lands though, we’ll have to wait and see.

Disclaimer

ETF Shares Management Limited ABN 77 680 639 963, AFSL: 562766. Investing involves risk and returns are not guaranteed. Refer to the relevant PDS and TMD available at www.etfshares.com.au