Trump’s 50% copper tariffs raise questions about winners and losers – and which direction the copper price will go. For Australian investors, they also raise questions about what it means for Rio and BHP.

We do not know what the final tariffs look like (what products they apply to, what exemptions will be made, if any). But based on current information, some answers are clear.

Big winner: Freeport McMoran

The biggest tariff winner is arguably Freeport McMoRan (FCX), the US copper miner. Freeport produces 60% of US refined copper and is vertically integrated – mining, refining, smelting – on US soil.

Thus far, the market has added a ~US$1 per pound premium to the US copper price (currently the market has priced in a roughly 25% premium to US copper, discussed below). According to Freeport’s annual report, its sensitivity to the copper price is such that a 10 cents per pound rise in copper prices translates into $135M extra EBITDA. So, assuming all its US-produced copper is sold in the US, an extra $1 comes in at a US$1.35B benefit for Freeport, roughly equal to its base dividend last financial year.

For Rio, US copper production (via Kennecott in Utah) accounts for 3 - 5% of overall revenues. BHP produces no copper in the US at all. For Rio and BHP, therefore, the positives stem more from Trump’s fast-tracking their proposed Resolution mine in Arizona in the context of these tariffs. This not only gives Resolution a higher probability of going ahead but also helps ensure it will be higher margin.

But even if Resolution does become one of the world’s largest copper mines, US copper will only ever be a small part of Rio and BHP – on both the supply and demand side.

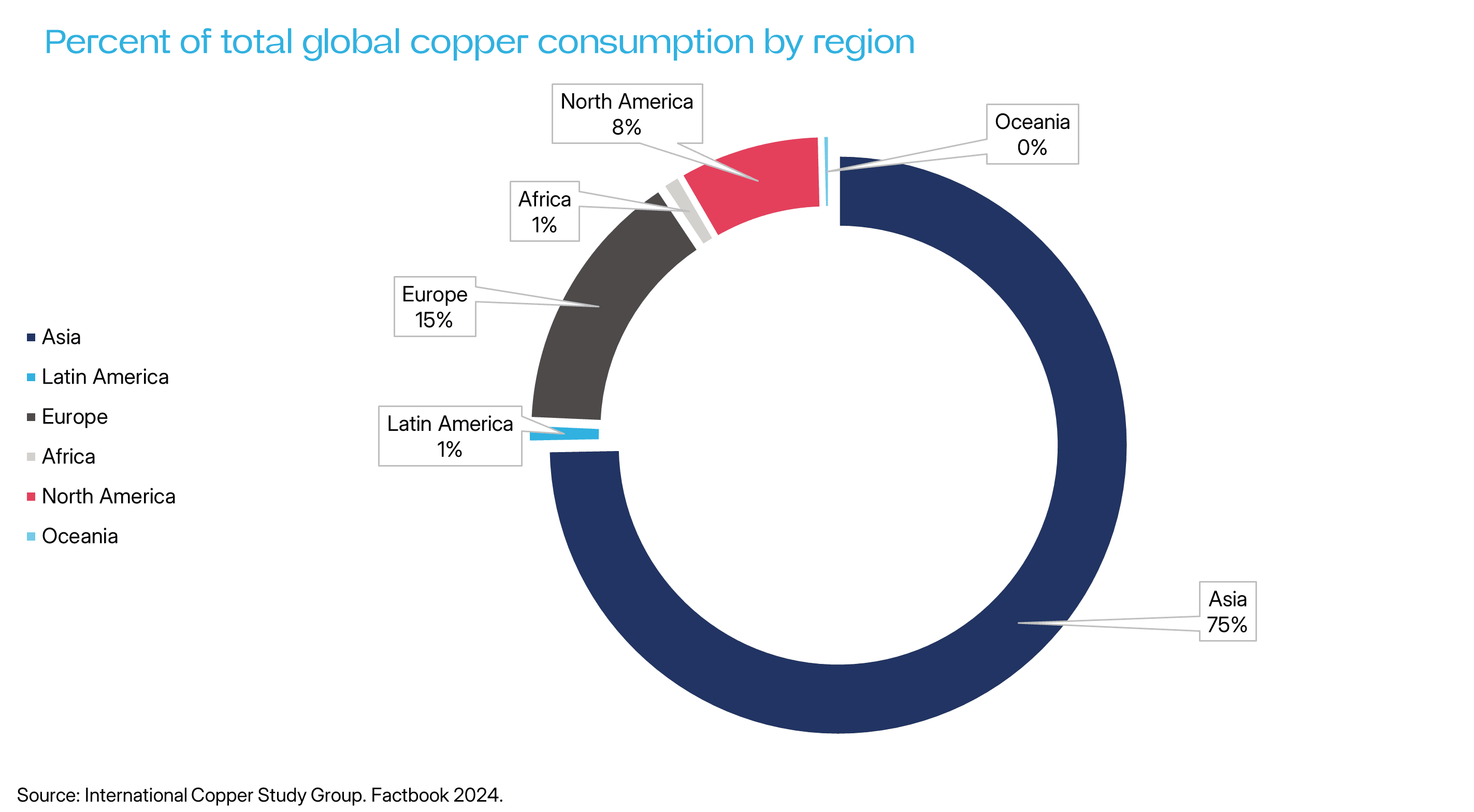

For demand: the US only accounts for 6% of global copper demand. Asia (China, India largely) makes up 75%.

For supply: scaling US copper mines is expensive. According to Greg Shearer at JP Morgan, one of the best metals analysts in the business, the weighted average incentive price for a US copper mine is US$5.10 (assuming a 15% IRR). This means copper prices need to stay above $5.10 per pound for an extended period to incentivise US production. While copper prices are US$5.40 per pound at the time of writing, there can be no assurance that they – or the tariffs driving them – can stay in place for years.

As such we suspect that the share price impact medium term from these tariffs will be modest for copper producers across the board, even Freeport.

Winner: Glencore and Trafigura

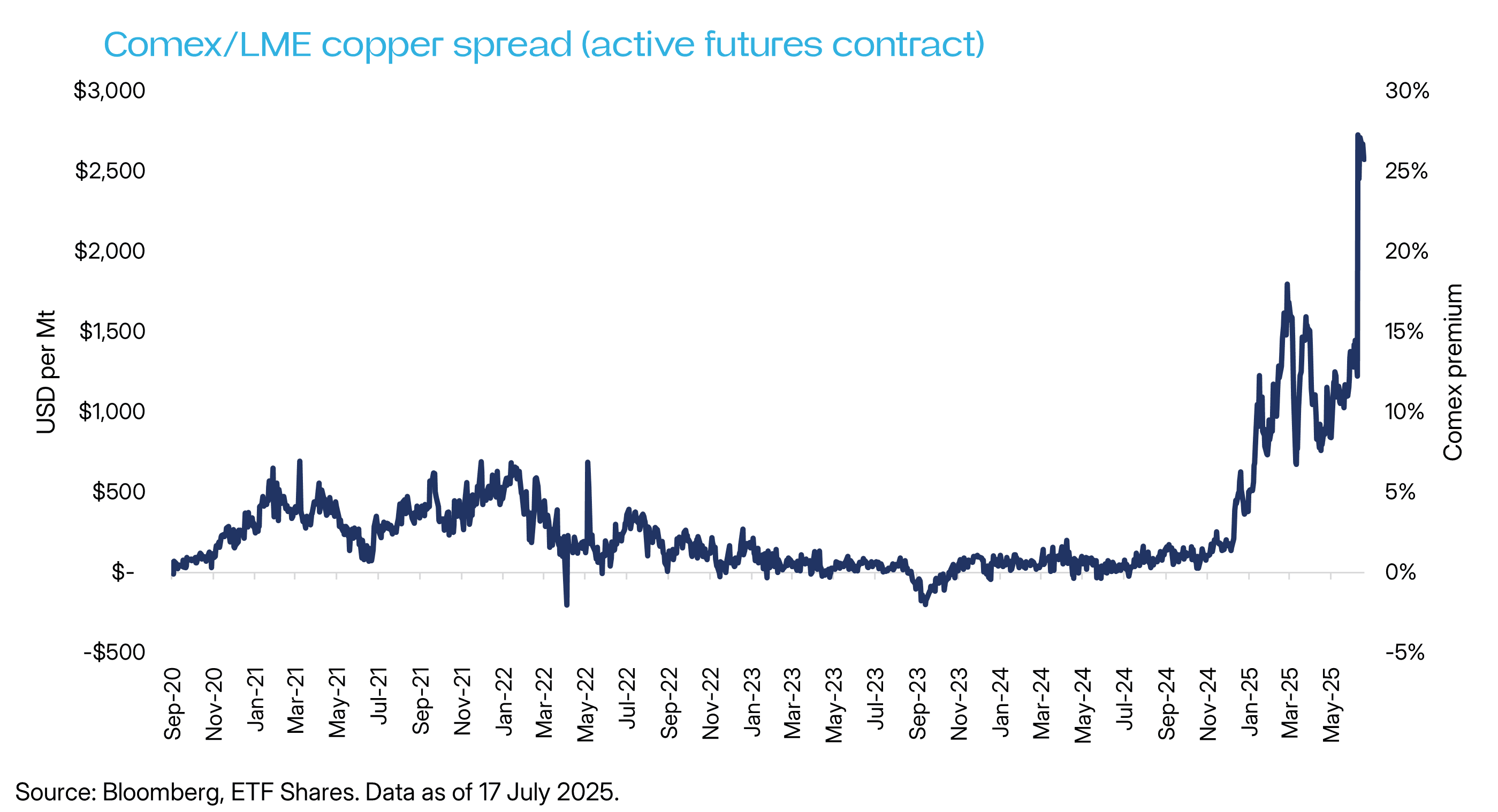

That copper traders are making a fortune on the arbitrage window between US and global copper prices has been well-reported. These tariffs mean copper traders can “buy low” copper in the international market, and “sell high” in the US as manufacturers pay a premium to stock up ahead of tariffs.

While the arbitrage window – that is, the difference between US and global copper prices - has widened to 27%, it remains below 50% - which is where it should be if tariffs were fully priced in.

In the short term, everyone expects that traders will continue to profit from this arbitrage window, and that the window will continue expanding towards 50% (thereby fully reflecting the tariff).

What will happen to the copper price?

Copper prices are strong now, but the current setup looks like a sugar hit in our opinion, with a hangover set to come in the second half of 2025.

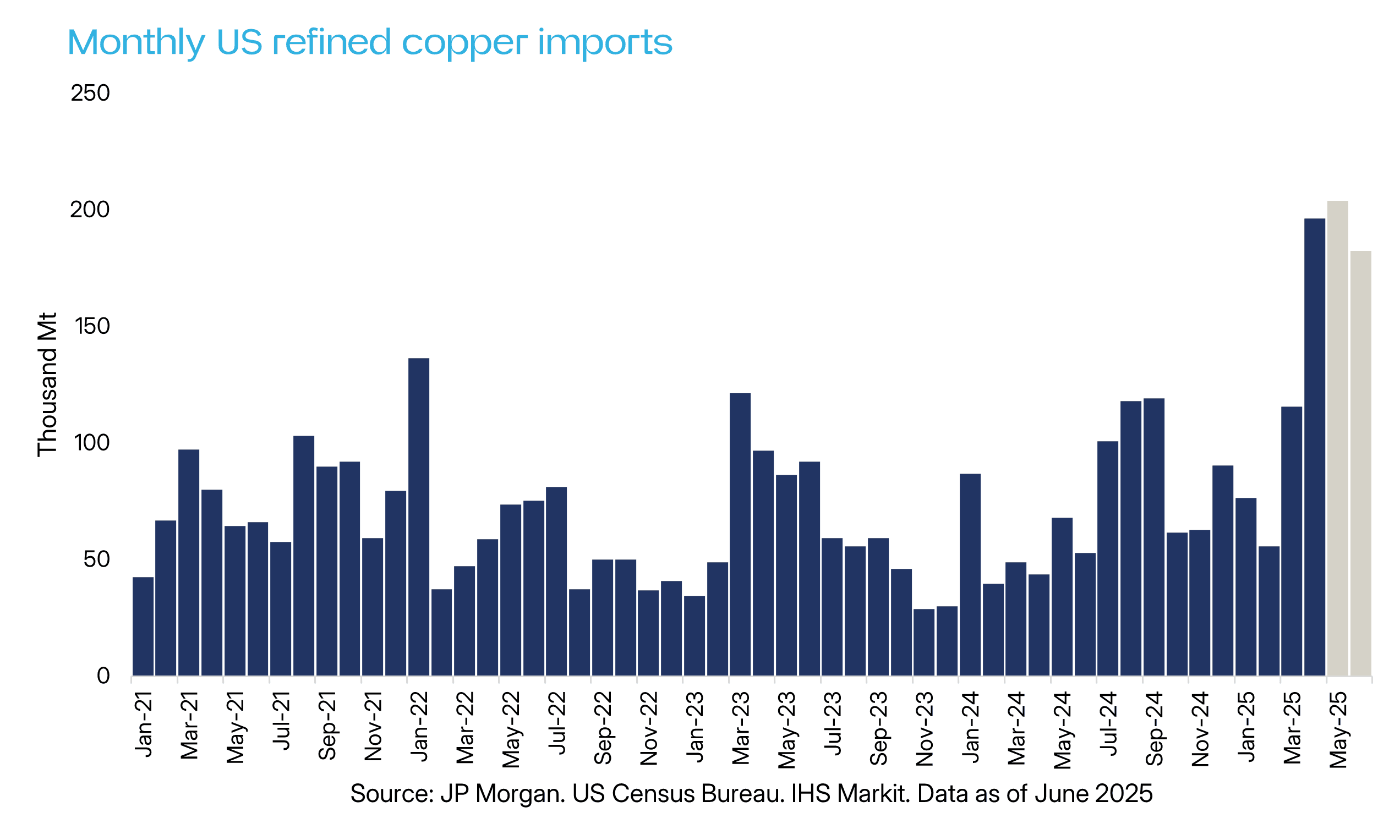

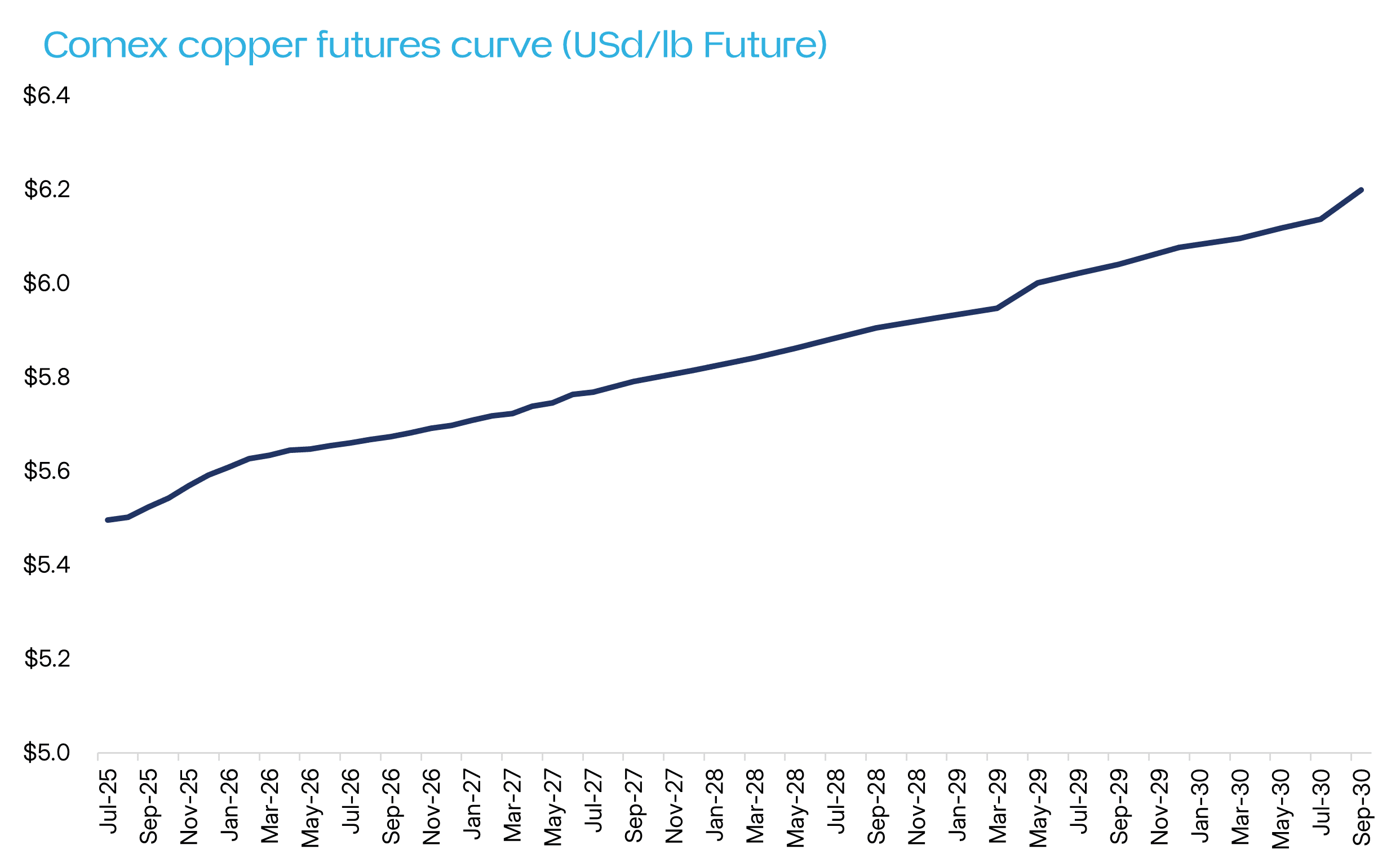

Traders have brought so much copper to the US that America now sits on enough warehoused copper to cover six months of import demand, according to JP Morgan. Indeed, copper has flooded the US to such an extent that traders are struggling to warehouse it. And they’ve done so in the context of a steep copper contango market, meaning they’re not under any financing pressure to sell.

As a result, a US copper glut is coming. Copper that would otherwise have gone to the US in H2 will likely head to other markets, pushing prices lower. Meanwhile, China has also frontloaded its own copper consumption in 2025. Demand from solar panels was pulled forward to get in front of tariffs while demand growth overall is muting.

In sum, data suggests the copper bull market has already run.